Facing a mountain of personal loan debt in 2026 can feel like a lonely battle. Between the high interest rates and the constant pressure from recovery agents, your mental peace often takes the biggest hit. However, if you are struggling to keep up with your EMIs, there is a legal and structured way out.

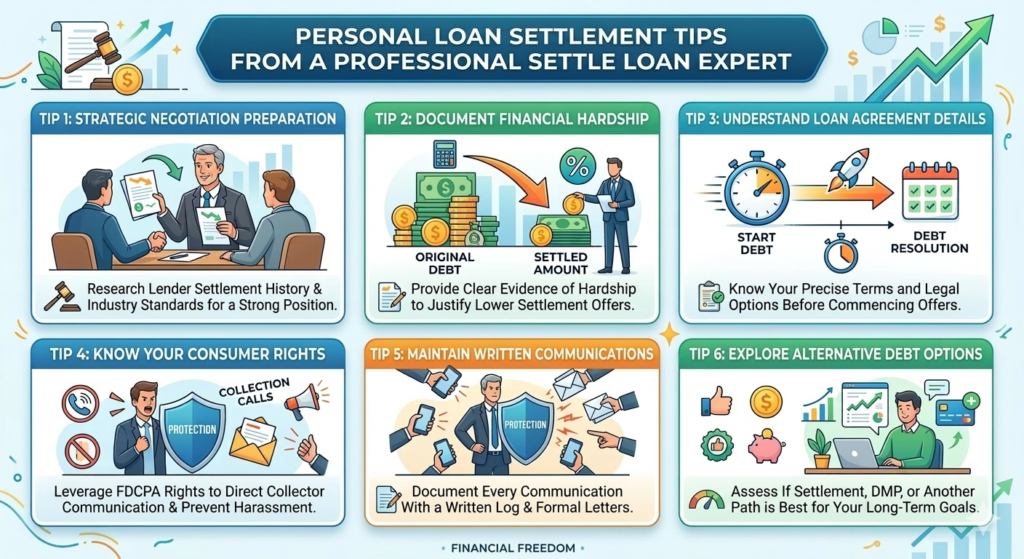

Choosing to settle loan accounts is a strategic decision that can save you from financial ruin. To help you navigate this complex process, we’ve gathered the top tips from a professional settle loan expert. By leveraging professional settle loan services and platforms like Loanifyr, you can reduce your debt by a massive margin and start fresh.

1. Understand the “Settlement Window”

The most important tip any settle loan expert will give you is regarding timing. Banks are businesses, and they only offer significant discounts when they believe they might lose the entire amount.

Usually, the best time to settle loan debt is after your account has been classified as a Non-Performing Asset (NPA). This typically happens after 90 days of non-payment. Once the account is in NPA, the bank is forced to set aside capital for that loss, making them much more willing to accept a lump-sum settlement of 30% to 50% of the total outstanding.

2. Stop Making Small “Token” Payments

A common mistake borrowers make is paying small amounts—like ₹2,000 or ₹5,000—just to keep the bank happy. A settle loan expert will tell you that this is often counterproductive.

- The Reason: These small payments only cover the “penal interest” and don’t reduce your principal. More importantly, they “reset” the clock on your delinquency, preventing the account from reaching the stage where a high-waiver settle loan agreement is possible.

3. Leverage Professional Settle Loan Services

Negotiating with a multi-billion rupee bank is intimidating. Banks have seasoned recovery teams whose job is to maximize their collection. By hiring professional settle loan services, you level the playing field.

Experts from platforms like Loanifyr act as a “Professional Firewall.” They handle all the aggressive calls and legal notices on your behalf. Under the 2026 RBI guidelines, once you are represented by a professional, the bank must direct all communication to your expert, effectively stopping the harassment at your home and workplace.

4. Build a “Hardship Portfolio”

To settle loan dues for the minimum possible amount, you must prove that you cannot pay, not just that you will not pay. A settle loan expert helps you compile a “Hardship Portfolio,” which includes:

- Medical Bills: Proof of health crises in the family.

- Job Loss Proof: Termination letters or bank statements showing zero income.

- Business Audit Reports: Showing a decline in revenue.Presenting this data professionally through settle loan services makes your request for a 70% waiver much more credible to the bank’s credit committee.

Comparison: DIY vs. Expert Negotiation

| Feature | DIY Negotiation | With a Settle Loan Expert |

| Average Discount | 10% – 25% | 50% – 75% |

| Legal Protection | Exposed to Harassment | Protected by Professional Firewall |

| Documentation | Prone to Loopholes | Legally Vetted OTS Sanction Letters |

| Success Rate | Moderate | High (Data-Driven) |

5. Never Pay Without an OTS Sanction Letter

One of the most dangerous traps in 2026 is paying a “settlement amount” based on a phone call or a WhatsApp message. A settle loan expert ensures you never part with your money until you receive an official One-Time Settlement (OTS) Sanction Letter.

This letter must be on the bank’s official letterhead and must include:

- The final agreed-upon amount.

- A “Full and Final” closure clause.

- A commitment to withdraw all legal cases (Section 138 or SARFAESI).Using Loanifyr ensures that your documentation is water-tight and that the bank cannot come back for more money later.

6. Planning for Credit Score Recovery

While you settle loan debt to escape immediate pressure, it does impact your CIBIL score. However, a settle loan expert doesn’t just leave you there. Professional settle loan services provide a 24-month roadmap for credit rebuilding. By using tools like secured credit cards or “credit-builder” loans, they help you restore your score to 750+, ensuring you are eligible for credit again in the future.

Conclusion: Take Back Your Financial Freedom

Personal loan debt can feel like a life sentence, but it doesn’t have to be. By following these expert tips and using professional settle loan services, you can resolve your debt for a fraction of the cost. You don’t have to face the recovery agents alone; an expert from Loanifyr can provide the shield and the strategy you need.

Reclaim your peace of mind and stop the cycle of stress today. If you are ready to settle loan debt on your own terms, visit Loanifyr for a free, confidential assessment of your situation. Let a dedicated settle loan expert handle the negotiations while you focus on rebuilding your life. Visit settle loan services now and take the first step toward becoming debt-free forever.