In the current financial landscape of 2026, many Indian borrowers find themselves caught in a relentless cycle of high-interest debt. Whether it is a personal loan that has become unmanageable due to job instability or credit card bills that have ballooned with penal interest, the pressure can be paralyzing. When monthly EMIs exceed your take-home pay, the dream of financial independence starts to feel like a distant memory.

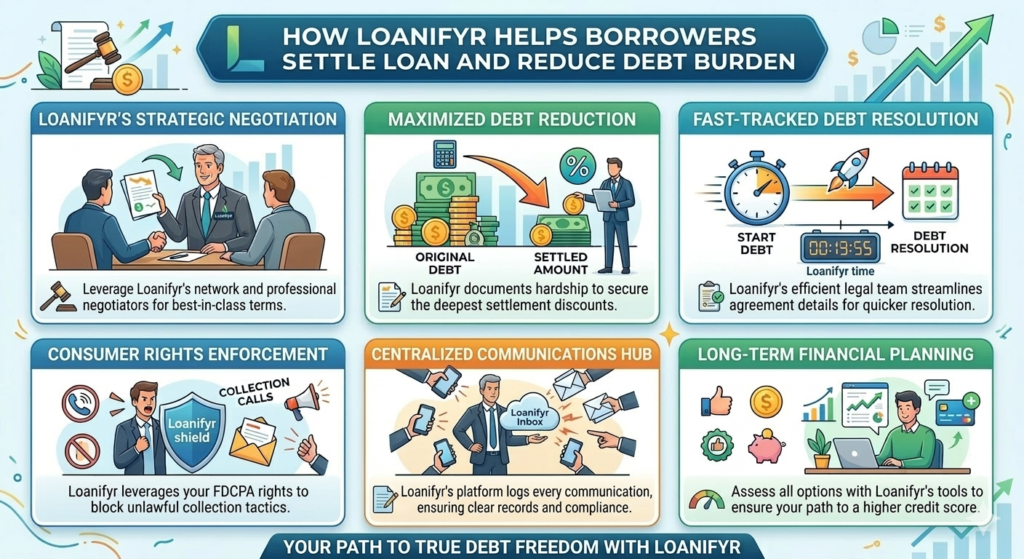

However, there is a strategic way to break these chains: the settle loan process. While banks often portray debt as an absolute obligation, the reality is that lenders are often willing to negotiate when they realize a borrower is in genuine distress. This is where Loanifyr steps in. By connecting borrowers with a dedicated settle loan expert, Loanifyr provides the professional leverage needed to resolve debt for a fraction of what is owed.

1. Professional Negotiation: The Loanifyr Edge

Negotiating with a multi-billion rupee bank is an intimidating task for the average person. Banks employ seasoned recovery teams whose sole objective is to maximize collection. When you attempt to settle loan accounts on your own, you are often met with rigid terms or measly 10% discounts.

Loanifyr changes the game by putting a settle loan expert in your corner. These experts understand the internal “bottom-line” of various banks and NBFCs. They use data-driven strategies to push for “haircuts” (discounts) ranging from 50% to 75%. By utilizing professional settle loan services, you transition from a position of weakness to one of strategic negotiation.

2. Timing the Settlement for Maximum Impact

One of the most critical aspects of debt resolution is timing. A settle loan expert from Loanifyr understands that banks are most flexible during specific windows, such as the “March Rush” at the end of the financial year or when an account reaches Non-Performing Asset (NPA) status.

By monitoring your delinquency cycle, Loanifyr ensures your proposal hits the bank manager’s desk at the exact moment they are most desperate to clear their books. This strategic timing is the difference between a minor discount and a massive waiver that clears lakhs of rupees off your balance.

3. Stopping Recovery Harassment

The psychological toll of debt is often exacerbated by aggressive recovery tactics. In 2026, the RBI has implemented strict guidelines regarding borrower dignity, yet many agents still cross the line.

When you hire settle loan services through Loanifyr, you gain an immediate “Professional Firewall.” Your settle loan expert sends a formal notice of representation to your creditors. Legally, once you are represented by a professional service, the bank must direct all communication to your representative. This puts an end to the constant phone calls and home visits, allowing you to focus on your work and family while Loanifyr handles the conflict.

4. Building a “Hardship Portfolio”

Banks do not grant settlements out of kindness; they do it based on risk assessment. To settle loan debt for the minimum possible amount, you must prove a genuine inability to pay. Loanifyr helps you compile a professional “Hardship Portfolio,” which includes:

- Income Evidence: Documented proof of salary cuts or job termination.

- Medical Records: Evidence of family health crises that depleted your savings.

- Financial Audits: A clear picture of your liabilities versus assets.

By presenting your case through a settle loan expert, you present a professional narrative that makes it easy for the bank’s credit committee to approve a high-waiver settlement.

Comparison: DIY Settlement vs. Using Loanifyr

| Feature | Negotiating on Your Own | Using a Loanifyr Settle Loan Expert |

| Typical Waiver | 10% – 25% | 50% – 75% |

| Legal Safety | High risk of “Willful Defaulter” tag | RBI-Compliant Legal Defense |

| Harassment | Direct and Constant | Immediate Professional Buffer |

| Documentation | Prone to bank-favored loopholes | 100% Vetted OTS Sanction Letters |

5. Legally Vetted Closure

A major pitfall in the settle loan process is making a payment without a proper One-Time Settlement (OTS) Sanction Letter. Loanifyr ensures that every rupee you pay is legally documented. Your settle loan expert meticulously reviews the bank’s offer to ensure it includes a “Full and Final” clause and a commitment to withdraw all active legal cases (such as Section 138 or SARFAESI notices).

6. A Roadmap to Future Credit

While a settlement does mark your credit report as “Settled,” Loanifyr doesn’t leave you after the payment. Professional settle loan services include a post-settlement roadmap for credit rebuilding. By guiding you through 2026-specific credit-builder tools, your settle loan expert helps you restore your CIBIL score to 750+ within 18 to 24 months, ensuring you aren’t barred from future financial opportunities.

Conclusion: Reclaim Your Peace of Mind

Debt is a financial obstacle, not a life sentence. With the expertise of Loanifyr and a dedicated settle loan expert, you can stop the stress and resolve your liabilities for the lowest possible amount. Professional settle loan services provide the shield and the strategy you need to win against big banks.

Don’t let another day of high interest and recovery stress pass you by. You can settle loan debt and start a new chapter today. Visit Loanifyr for a free, confidential assessment of your situation. Let a professional handle the negotiations so you can focus on your future. Visit settle loan services now and take the first step toward a debt-free life.