When financial hardship hits, your monthly loan commitments can quickly transform from manageable payments into overwhelming burdens. In India, borrowers facing such distress often find themselves at a crossroads between two primary debt-relief options: EMI restructuring and opting for settle loan services.

While both paths aim to provide relief, they function very differently and have vastly different long-term consequences for your credit health. This guide breaks down the key differences to help you decide which is right for your situation.

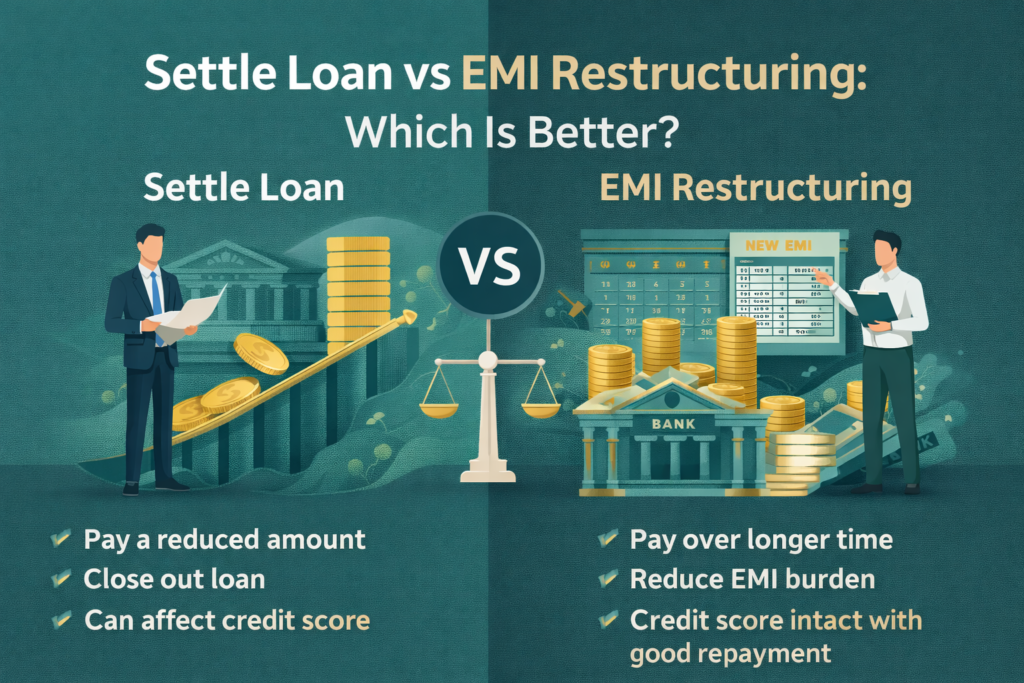

What is EMI Restructuring?

EMI restructuring (also known as loan rescheduling) is a process where the lender modifies the existing terms of your loan to make repayments easier. This is typically done without closing the account. Common methods include:

- Tenure Extension: Increasing the loan period to reduce the monthly EMI amount.

- Moratorium Period: A temporary “payment holiday” where you don’t pay EMIs for a few months (though interest may still accrue).

- Interest Rate Reduction: In rare cases of extreme hardship, a bank might lower the interest rate to help you stay current.

Best for: Borrowers experiencing a temporary financial setback (like a 3-month medical leave or a job transition) who still have the intent and future capacity to pay back the full amount.

What are Settle Loan Services?

A loan settle (or One-Time Settlement) is a negotiation where the lender agrees to accept a lump-sum payment that is significantly less than the total outstanding balance. Once this amount is paid, the lender “forgives” the rest and closes the account.

Because negotiating with banks is complex, many people hire professional loan settlement services. These agencies use legal expertise and negotiation tactics to:

- Stop Recovery Harassment: They act as a legal buffer between you and recovery agents.

- Maximize Discounts: They know the “haircuts” banks are willing to take, often saving you 30% to 70% of the debt.

- Ensure Legal Closure: They verify that the bank issues a proper Settlement Letter and No Dues Certificate.

Best for: Borrowers facing permanent or severe financial distress (like total business failure or permanent disability) who cannot realistically pay back the full principal.

Key Differences at a Glance

| Feature | EMI Restructuring | Loan Settlement |

| Total Amount Paid | Full amount (plus extra interest due to tenure) | Reduced amount (30%–70% discount) |

| Credit Score Impact | Minimal (10–25 point dip) | Severe (75–150 point drop) |

| Credit Report Status | Marked as “Restructured” | Marked as “Settled” |

| Future Loan Eligibility | High (after a few timely payments) | Very Low (for the next 5–7 years) |

| Payment Mode | Continued monthly EMIs | One-time lump sum |

Comparing the Pros and Cons

EMI Restructuring

- Pros: It protects your financial reputation. Your account remains “standard” or “restructured,” which is seen as a responsible way to manage a crisis. It keeps the door open for future home or car loans.

- Cons: You end up paying more in the long run. By extending the tenure, the total interest component of the loan increases.

Loan Settlement

- Pros: It offers immediate, massive debt reduction and stops the cycle of interest and penalties. It provides a clean break from a debt you can never pay back. Professional loan settlement services also provide protection against aggressive recovery tactics.

- Cons: The “Settled” tag is a major red flag on your CIBIL report. It tells future lenders that you didn’t fulfill your original promise, making it very difficult to get new credit for several years.

Which Should You Choose?

The decision between a loan settle and restructuring depends entirely on your recovery timeline.

Choose EMI Restructuring if:

- Your income has dropped temporarily, but you expect it to recover soon.

- You want to buy a house or car in the next 3–5 years and need a high credit score.

- The bank is willing to extend your tenure to an EMI amount you can afford today.

Choose Settle Loan Services if:

- You have no source of income and no prospect of paying the full debt.

- You are being harassed by recovery agents and need legal protection.

- You have access to a small lump sum (perhaps from family or selling an asset) that can end the debt forever.

Conclusion

While restructuring is the “cleaner” option, it isn’t always possible for those in deep financial crises. If you are truly unable to pay, loan settlement services provide a legal, structured way to exit debt and stop the mental toll of constant collections. It allows you to trade a few years of “credit invisibility” for immediate financial survival.